At A Glance:

What: Brownsburg Community School Corporation seeks to close short-term funding gaps and avoid a 2026 referendum by partnering with the Town of Brownsburg, Brown and Lincoln Townships.

What: Joint Town Council & RDC Meeting – May 14th, 2026, 6:00pm – Town Hall

What: Joint Brown & Lincoln Township Meeting – May 19th, 2026 6:30pm – Town Hall

What: Information how to contact your public servants is listed near the bottom of this article.

Summary:

Brownsburg schools face a multi-million-dollar funding gap caused by recent state legislation and tax cuts. The Brownsburg Community School Corporation (BCSC) has already cut costs, has turned to local taxing entities for additional temporary support. Town and township officials are negotiating contributions that could prevent a 2026 referendum, though a vote may still be necessary in 2028 if state funding does not improve. BCSC must secure alternative funding before the referendum filing deadline of June 1st 2026.

The Town of Brownsburg is also facing financial impacts from this legislation, and an overview of the Town’s position is included in this article.

![]()

![]()

A Brief Look Back, How We Got Here

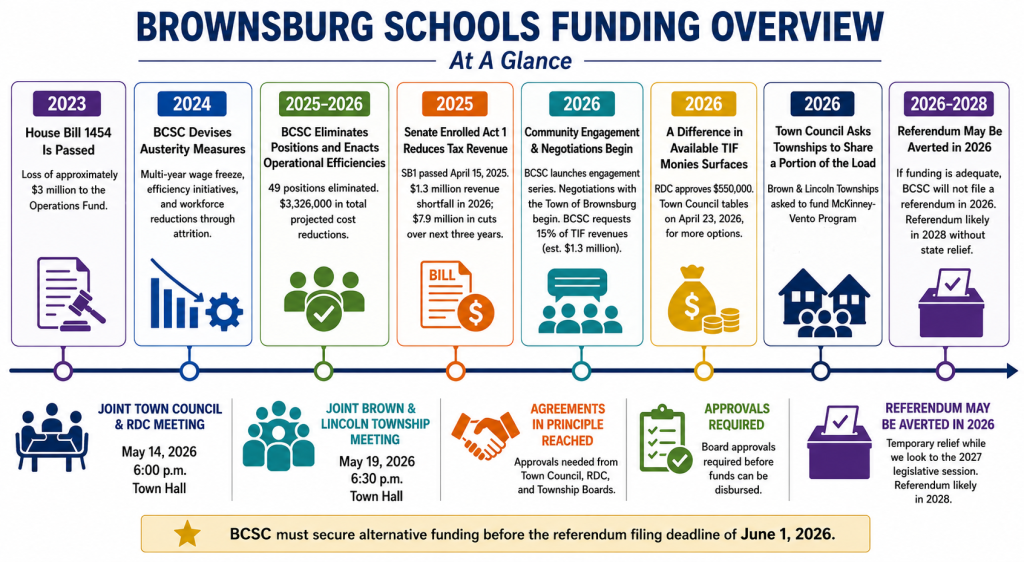

2023 House Bill 1454 Is Passed

This discontinued the option of seeking an exemption from the Department of Local Government Finance (DLGF), where the DLGF confirmed eligibility within prescribed guidelines, they then dictate the surplus monies BCSC could transfer between capital and operating funds. This resulted in a loss of approximately 3 million to the operations fund.

![]()

2024 BCSC Devises Austerity Measures

BCSC executive staff has implemented austerity measures, including an organization wide multi-year wage freeze, operational efficiency initiatives, and workforce reductions through attrition. With school board approval, transfers from the Education Fund to the Operations Fund may be incrementally increased, from 5.5% each year, up to an amount to mitigate revenue losses from HB 1454. Program rollout begins in 2025 with completion scheduled for 2026.![]()

2025-2026 BCSC Eliminates Positions and Enacts Operational Efficiencies

BCSC eliminated 49 positions for 2026–27, generating $2,438,000 in personnel savings across certified staff, educational support staff, and operations support staff.

Additional operational and one-time savings total $990,000.

Bringing total projected cost reductions to $3,326,000.

Given the aforementioned, BCSC felt they had weathered the budgetary storm.

![]()

2025 Senate Enrolled Act 1 Reduces Tax Revenue

Senate Enrolled Act 1 commonly known as SB1 passed on April 15, 2025, which included current year and future property tax cuts. It impacts all municipalities, school corporations, fire territories, among government entities. This legislation was enacted after BCSC budgets were submitted to the DLGF. This results in a 1.3-million revenue shortfall. BCSC estimates $7.9 million in cuts over the next three years. BCSC realizes the loss of revenue outweighs earlier mitigations and seeks additional short term revenue sources.

![]()

2026 BCSC Begins Community Engagement Series and Negotiations with Town of Brownsburg Begin

BCSC rolls out their Community Engagement Series. Included within their program was a call to action asking the public to contact the Indiana state legislators to carve out an exception to HB1454 for school systems similar to BCSC who are in like circumstances. BCSC viewed this was an easy stopgap measure to replace funding lost by SB1. The short legislative session was primarily focused on redistricting, no action was taken to address BCSC and like districts budgetary woes.

The series also include information on which areas would be reviewed if additional cuts were necessary. Being on this list is NOT an indication cuts will occur, just that these areas are first for further scrutiny.

Following the failure by the Indiana State Legislature to act, BCSC publicly announces their intention to seek 15% of Town of Brownsburg Tax Increment Finance (TIF) revenues. This first-of-its-kind request is in alignment with Indiana State Law. BCSC publishes their estimate that 1.3 million are eligible for transfer.

![]()

2026 A Difference in Available TIF Monies Surfaces

The Town of Brownsburg Redevelopment Commission (RDC) offers $550,000. The $1.3 million figure BCSC used represents the maximum amount the Commission could legally provide under Indiana’s 15% TIF statute based on eligible 2025 revenues. The Commission instead offered $550,000 because it says significant debt obligations, reserve requirements, future capital projects, refinancing risks, and anticipated revenue losses from SEA 1 require the Town to retain more TIF funds for financial stability.

At the April 16, 2026 RDC meeting $550,000 is approved. The RDC suggests the Town Council is better positioned to adjust the number up or down as the measure is forwarded to them for approval. The town council tabled the same matter on April 23rd, 2026, noting more time was needed to explore additional funding options.

![]()

2026 The Town Council Asks the Townships to Share a Portion of the Load

Members of the Brownsburg Town Council initiated discussions with the Lincoln and Brown Township Trustees to explore financial support options for BCSC to help avoid a referendum. Following multiple legal reviews, BCSC requested assistance for the McKinney-Vento program, an unfunded Federal mandate from the Reagan Administration, which provides transportation and educational continuity for students experiencing homelessness, even when temporary housing places them outside district boundaries. The transportation cost for the program is approximately $315,000 annually. BCSC seeks a three-year financial commitment from the townships to help sustain this mandated service.

Town of Brownsburg Faces Its Own Fiscal Pressures

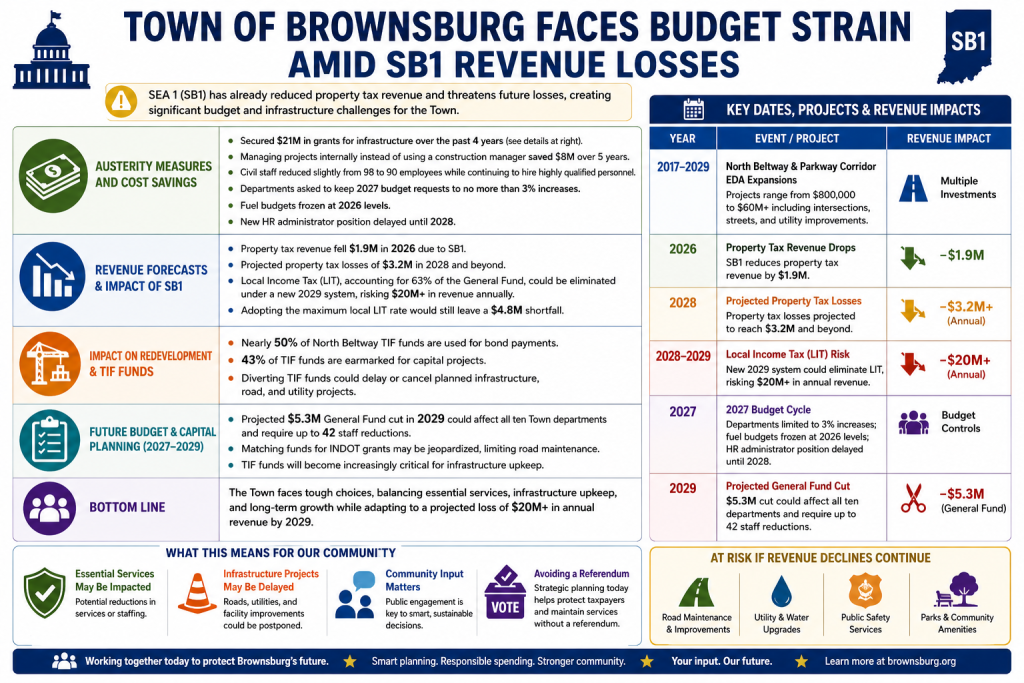

Town of Brownsburg Faces Budget Strain Amid SB1 Revenue Losses

The Town of Brownsburg is preparing for significant financial challenges following the passage of Indiana SEA 1 (SB1), which has already reduced property tax revenue and threatens future losses.![]()

Austerity Measures and Cost Savings

Town officials say Brownsburg has already implemented multiple cost-saving strategies while aggressively pursuing outside funding for infrastructure projects.

- Secured nearly $21 million in grants over four years, including major funding from the American Rescue Plan, INDOT, and the Indiana Finance Authority.

- Saved an estimated $8 million over five years by managing projects internally rather than using outside construction managers.

- Departments were asked to limit 2027 budget increases to 3% or less, while staffing and hiring growth have been restricted.

Revenue Forecasts

Town officials project millions in future revenue losses tied to declining property tax collections and changes to Local Income Tax distributions.

- Brownsburg lost approximately $1.9 million in property tax revenue in 2026, with projected losses growing to $3.2 million annually beginning in 2028.

- Changes to the Local Income Tax (LIT) system in 2029 could reduce Town revenues by more than $20 million annually.

- Even adopting the maximum local LIT rate could still leave a projected $4.8 million shortfall.

Impact on Redevelopment and TIF Funds

Town officials say TIF revenues are already heavily committed to debt obligations and future infrastructure projects.

- Nearly 50% of North Beltway TIF revenues are dedicated to bond payments, with most remaining funds already planned for capital projects.

- Officials warn diverting TIF dollars could delay or eliminate future infrastructure, utility, and roadway improvements.

Future Budget and Capital Planning (2027–2029)

Projected revenue declines could significantly impact staffing, infrastructure maintenance, and future capital projects.

- A projected $5.3 million General Fund reduction in 2029 could impact all ten Town departments and potentially affect up to 42 staff positions.

- Reduced matching funds may limit Brownsburg’s ability to secure future INDOT infrastructure grants and maintain road improvement schedules.

THAT BRINGS US TO TODAY

Agreements in Principle Reached; Approvals Needed; Joint Meetings Scheduled

The Town Council has scheduled a joint Council and RDC meeting scheduled for May 14th at 6:00pm. The RDC approved as presented $550,000 at their April 16th, 2026 meeting. During the joint meeting on the 14th the amount of TIF monies contributed to BCSC may be adjusted up or down. Additional requests may be added, including a contractual agreement not to file a referendum if monies are allocated. In the event an adequate funding amount and related items are approved by the Town Council and RDC, the combined townships are next to act.A Combined Brown Township and Lincoln Township Meeting including their respective boards is scheduled for May 19th 2026 6:30pm. To discuss what if any funding they will contribute to BCSC.Township Trustees have agreed in principle to fund portions of BCSCs McKinney-Vento program Homeless Children and Youth Program. This program aligns with the mission of the Township Trustee; and has received favorable legal guidance from their respective retained counsels and the Indiana State Board of Accounts (SBOA). The SBOA is charged with oversight in this matter. Both Trustees seek written assurance BCSC will not seek a referendum in 2026. Board approval is required to before funds can be disbursed.

Referendum Maybe Adverted in 2026

If monies contributed by the Town of Brownsburg, Brown and Lincoln Townships are adequate, BCSC has agreed not to file a referendum in 2026. This action gives BCSC a temporary respite and provides time for BCSC to determine what if any relief may come from the upcoming 2027 Indiana state legislative session. Any budgetary reforms must be reviewed and approved by Jeff Thompson Chairman of the House Ways and Means Committee.Barring any significant changes from the 2027 session, using current BCSC revenue and expense projections a referendum is all but inevitable in 2028.

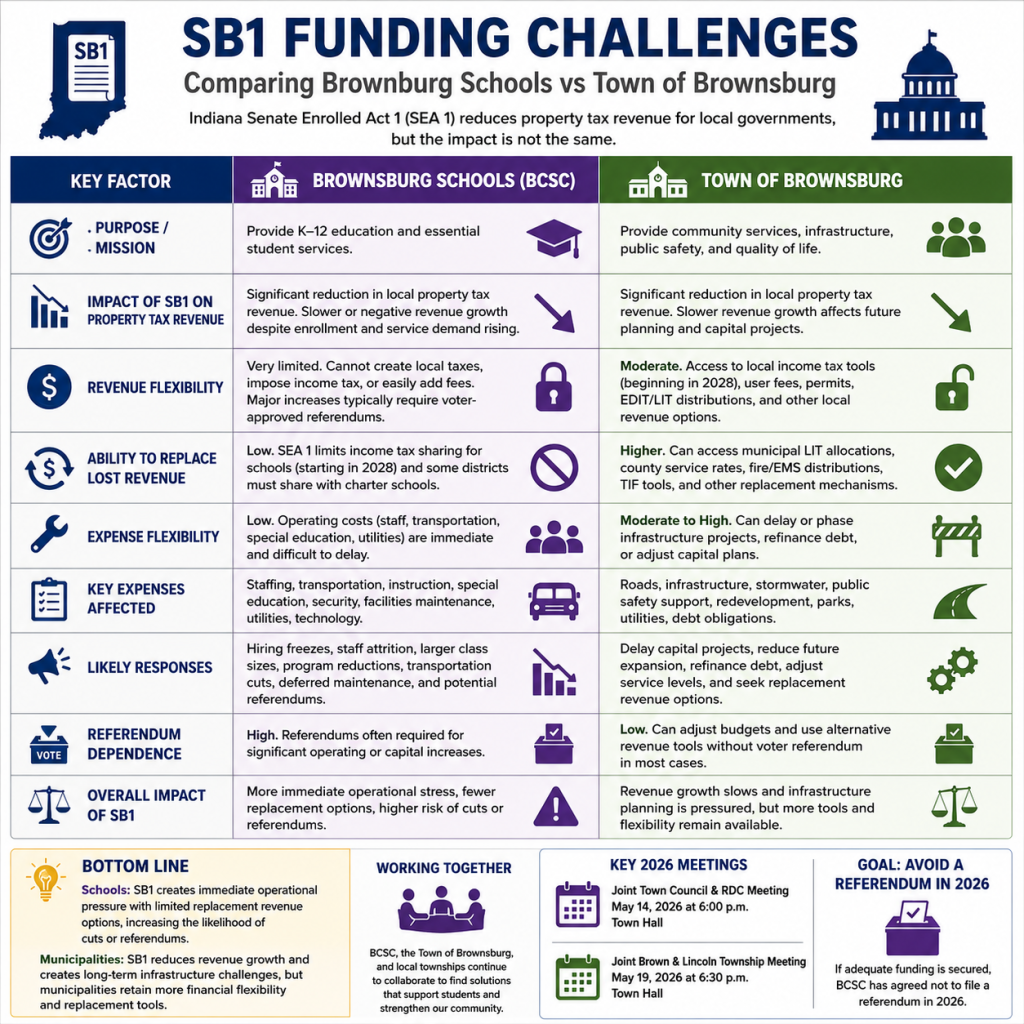

The Larger SEA 1 Debate

Summary:

Brownsburg Town and Brownsburg School’s now finds themselves balancing competing financial pressures affecting one another. Both entitles have highlighted broader statewide concerns regarding how SEA 1 affects their respective organizations.

Central Issues:

- Schools argue operational pressures are immediate and severe.

- Municipalities argue infrastructure obligations remain substantial despite reduced revenue growth.

- Both entities claim existing financial pressures are legitimate and long-term.

The debate has become increasingly difficult because both sides are attempting to preserve essential public services while adapting to reduced future revenue growth.

Point / Counter Point

There are citizens who are opposed to the revenue sharing between the Town of Brownsburg, Brown and Lincoln townships and the schools. Their viewpoints follow:

![]()

Letter to the Editor –

As Brownsburg debates additional financial assistance for BCSC, much of the conversation has focused on protecting schools from further cuts. But far less attention has been given to the financial pressures already facing the Town of Brownsburg itself.

The Town receives a much smaller share of local property tax revenue than BCSC, yet it remains responsible for roads, storm-water systems, utilities, sewer infrastructure, redevelopment projects, and managing continued growth across the community. Town officials have publicly discussed nearly $50 million in future infrastructure and capital improvement needs.

This is why the TIF debate matters.

BCSC has argued roughly $1.3 million could legally be transferred under Indiana’s 15% TIF statute. RDC officials counter that after debt obligations, reserves, and existing infrastructure commitments are accounted for, the realistic amount available is much closer to the $550,000 already approved.

Supporters of the Town’s position argue these are not unused surplus dollars. Those funds are already tied to long-term infrastructure obligations that directly affect traffic, drainage, utilities, development, and public services throughout Brownsburg.

No one disputes that BCSC faces real financial challenges following recent state tax changes. But many residents are asking whether the Town is now being placed in an impossible position — expected to absorb additional financial strain while managing its own long-term obligations.

Schools and infrastructure are both essential to Brownsburg’s future. The community deserves an honest discussion about the financial realities facing BOTH before divisions deepen over future funding or a possible referendum.

![]() Dear Brownsburg Sentinel Editor –

Dear Brownsburg Sentinel Editor –

Using Township Funds for Education is Cheating The System

BCSC funding concerns should be separated from emotion and viewed through the lens of government accountability and taxpayer trust.

Township governments and school corporations are separate taxing entities with separate legal responsibilities under Indiana law. Township taxes were collected and approved by taxpayers for township purposes — not to backfill school corporation budget shortfalls.

That distinction matters. Every government unit submits budgets based on its own statutory responsibilities, and taxpayers are told where their money is going. Redirecting those funds after collection raises serious concerns about transparency, accountability, and whether taxpayers are being asked to support uses they never approved. The process is the same for every taxing entity – including school corporations and township governments.

This debate also should not become about whether someone “supports schools” or “cares about children.” Many residents can support education while still questioning whether shifting money between government units is appropriate or lawful.

If BCSC truly needs additional long-term funding, Indiana law already provides a mechanism: a public referendum where taxpayers directly decide whether they support additional school funding. That process may be difficult politically, but it is transparent and accountable. Attempts to avoid that process circumvents the intent of Indiana law, just as transferring funds between taxing entities violates the State budget review system that protects taxpayers from runaway government spending.

Avoiding that process by transferring township funds only delays the larger funding conversation and risks damaging public trust in local government.

Email Your Public Servants – Let Your Voice Be Heard

RDC@brownsburg.org – All Members of the Town of Brownsburg RDC

towncouncil@brownsburg.org – All Members of the Brownsburg Town Council

spatterson@mylincolntownship.com – Steve Patterson Lincoln Township Trustee

browntownshipin@gmail.com– Angela Delp – Brown Township Trustee

State Legislature

H28@iga.in.gov – Jeff Thompson – Chairman of the House Ways and Means Committee

Meeting Agendas

>> Click Here << For the Joint Town Council RDC Meeting Packet

>> Click Here << For the Joint Brown & Lincoln Township Meeting Agenda

Resources Referenced In This Article

>> Click Here << Brownsburg Schools Community Engagement Series

>> Click Here << DLFG Information on Filing a Referendum

>> Click Here << An Explanation of Tax Increment Finance (TIF) Districts

>> Click Here << McKinney-Vento program Homeless Children and Youth Program

Content courtesy of:

Article by The Editor

Brownsburg Community Schools Corporation – Community Engagement Series

{kind=link}